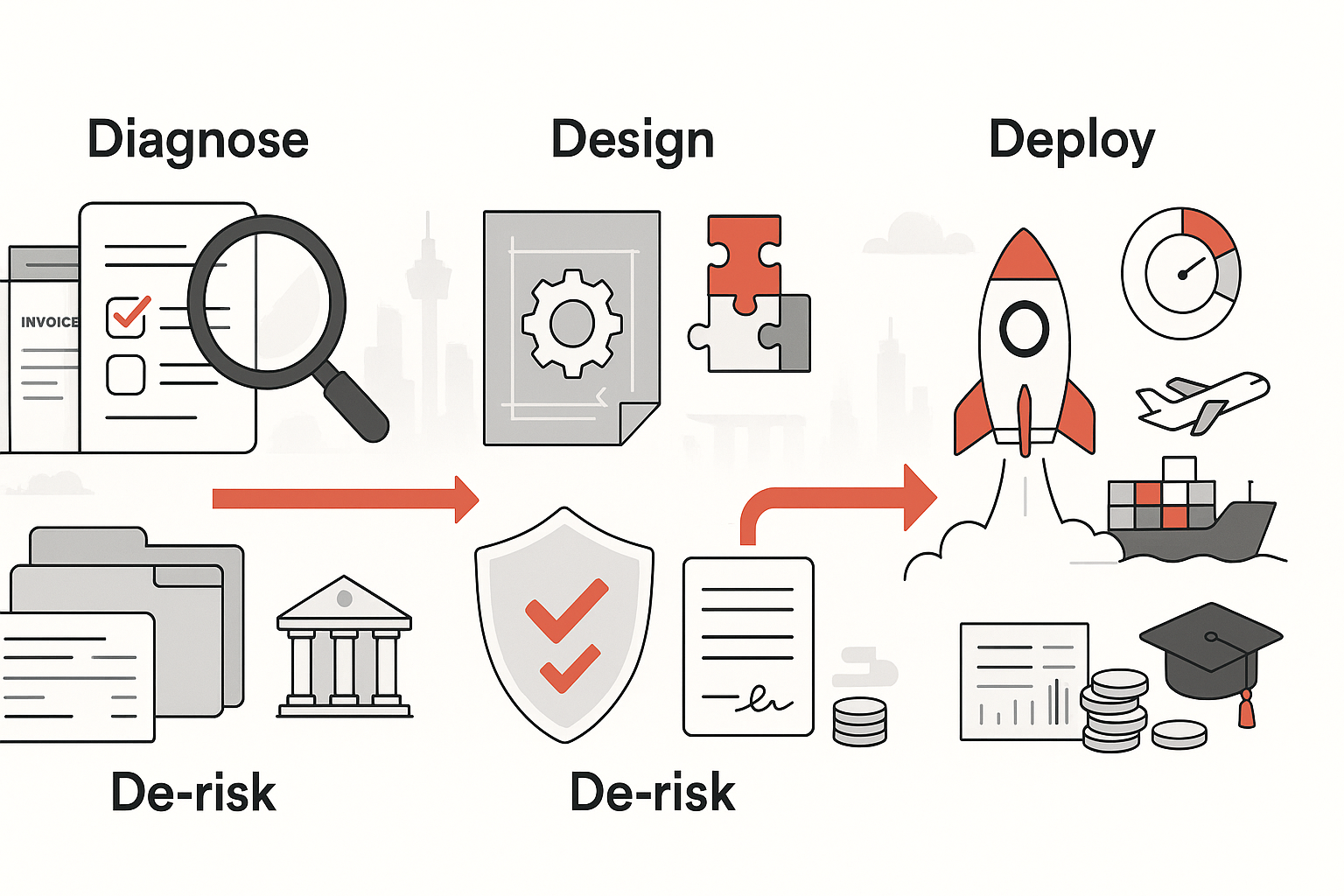

Bankability is less a status and more a set of habits. In Singapore, where financial institutions operate with prudence, SMEs that codify these habits tend to outcompete on access and price. The journey starts with clean numbers and ends with a diversified capital stack aligned to business rhythm.

First, institutionalize financial hygiene. Close your books monthly, reconcile cash, and maintain rolling cash forecasts. Track cohort-level revenue, gross margin trends, and customer concentration. Establish separate business banking, pay yourself a predictable salary, and document shareholder loans formally. This clarity allows lenders and investors to evaluate risk without decoding ambiguity.

Second, align instrument to purpose. Working capital swings are best served by overdrafts, revolving credit, or invoice finance. Durable assets—machinery, vehicles, store fit-outs—fit term loans or asset finance with tenors matching useful life. Experimentation and market entry, where returns are uncertain, merit equity or convertible notes. For seasonality, revenue-based facilities can smooth cash burdens. This match-making reduces default risk and earns better pricing.

Third, negotiate intelligently. Beyond interest rates, scrutinize fees, amortization profiles, covenants, cross-default clauses, and personal guarantees. Seek covenants you can monitor monthly. Clarify cure periods. Ask for prepayment flexibility if you anticipate early payoff. Compare lenders’ monitoring expectations with your reporting capabilities to avoid administrative drag.

Fourth, use credibility multipliers. Audited statements, reputable directors or advisors, and stable governance structures reduce perceived risk. Insurance on key assets and receivables can substitute for hard collateral in some cases. Letters of intent, framework agreements, or recurring revenue evidence can strengthen applications for asset-light companies.

Fifth, cultivate relationships. Proactive updates to bankers and alternative lenders—quarterly summaries, major contracts, and risk mitigations—build trust before an application lands. Cycle through smaller facilities cleanly to prove repayment discipline. Over time, this track record compresses spreads and increases limits, turning bankability into a compounding advantage.

Consider capital as a portfolio. Blend low-cost senior debt for predictable needs, flexible short-tenor instruments for gaps, and selective equity for step-changes. Maintain headroom to absorb shocks; model a downside case where revenue falls and still meets debt service. Avoid stacking multiple high-cost products that trap free cash in fees and rigid schedules.

Finally, tell a coherent story. A crisp use-of-funds memo, unit economics that scale, and a repayment path grounded in conservative assumptions signal professionalism. Pair this with operational levers—improved collections, negotiated supplier terms, inventory discipline—to show control over cash drivers.

When SMEs adopt these practices, the financing barrier becomes permeable. In Singapore’s trust-centric ecosystem, disciplined transparency and wise instrument selection are the fastest routes from “not yet” to “approved.”